The 2015 Spending Review set out the NHS funding settlement for the rest of the parliament including the funding allocated to the NHS in 2017/18.

The government has argued that, in looking at future NHS funding, the focus should be on ‘NHS frontline funding’ – the amount allocated to NHS England. The health select committee and other commentators, such as The King's Fund, Nuffield Trust and Health Foundation, have argued that the focus should be on the total Department of Health (DH) spending allocation as there have been substantial cuts to the non-NHS England element of DH spending, making the increase in the overall DH departmental allocation significantly lower. In the analysis below, we have deliberately used the government’s preferred measure of NHS England allocation, even though we know that providers are adversely affected by the reductions in the wider DH budget (for example, providers have been adversely financially affected by non-NHS England cuts to Public Health England which equate to cuts of 3.9% per year until 2020/21). Overall we have sought to take a conservative approach.

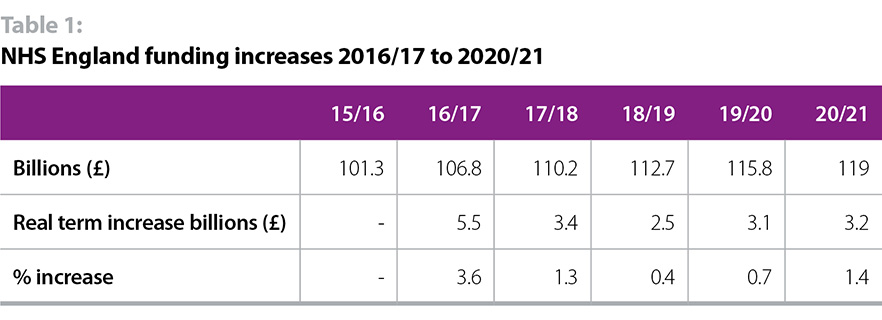

The table below sets out the NHS England funding increases between 2016/17 and 2020/21 announced in the Spending Review:

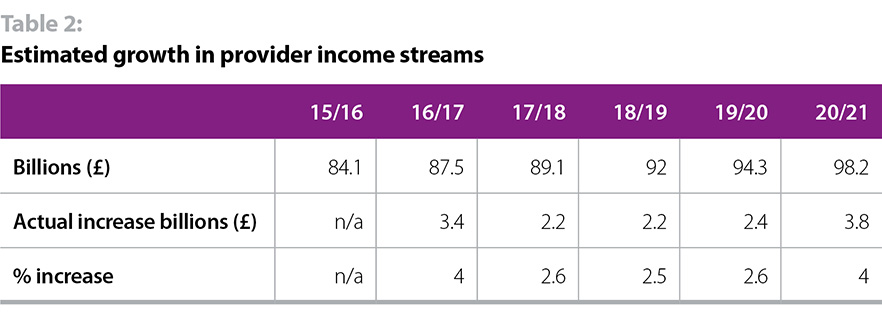

Within NHS England’s 1.3% real terms 2017/18 funding increase, actual CCG allocations (the primary source of NHS provider sector funding) will increase by 2.1% and specialised commissioning spend (a second source of NHS provider sector funding) will increase by 4.8%. Taken together total commissioning spend therefore increases by 2.6% overall. For the provider sector this represents the following estimated growth in income streams:

(Due to inability to disaggregate, the table shows the increases for all spending on frontline NHS provision: NHS trusts, private providers delivering NHS treatments and CCG prescribing and admin costs. Given that NHS provider funding accounts for by far the largest share of this spend, it is reasonable to assume the percentage increase applies to NHS provider income.)

This settlement has a number of well known features:

- The average overall real terms annual increase in NHS England funding across the life of this parliament is 1% per year, significantly below the NHS historical average and the assumptions around NHS cost and demand growth of between 4% and 5.5% (see assumptions for 2017/18 in section on cost and demand increase).

- The settlement was described by Simon Stevens, chief executive of NHS England, as a U bend given that it was deliberately front loaded, with the largest increase in the current financial year with significantly lower funding increases in the middle years of 2017/18 to 2019/20.

- From the day the settlement was announced, commentators have pointed to the difficulty the NHS would have in the middle years of the settlement. Simon Stevens told the public accounts committee that “… we got less than we asked for in that process. So I think it would be stretching it to say that the NHS has got more than it has asked for.”

Now that the NHS has reached the middle years of the U bend, it is no great surprise that it faces challenges in trying to deliver what is required of it, given the sharply lower funding increases.